Before: The Honourable Mr. Justice Truscott

Reasons for Judgment

| Counsel for the plaintiff: |

B.J. Lotzkar |

| Counsel for the defendant: |

D.A. Crawford |

|

Date and Place of Trial/Hearing: |

October 25 and 26, 2006 |

|

|

New Westminster, B.C. |

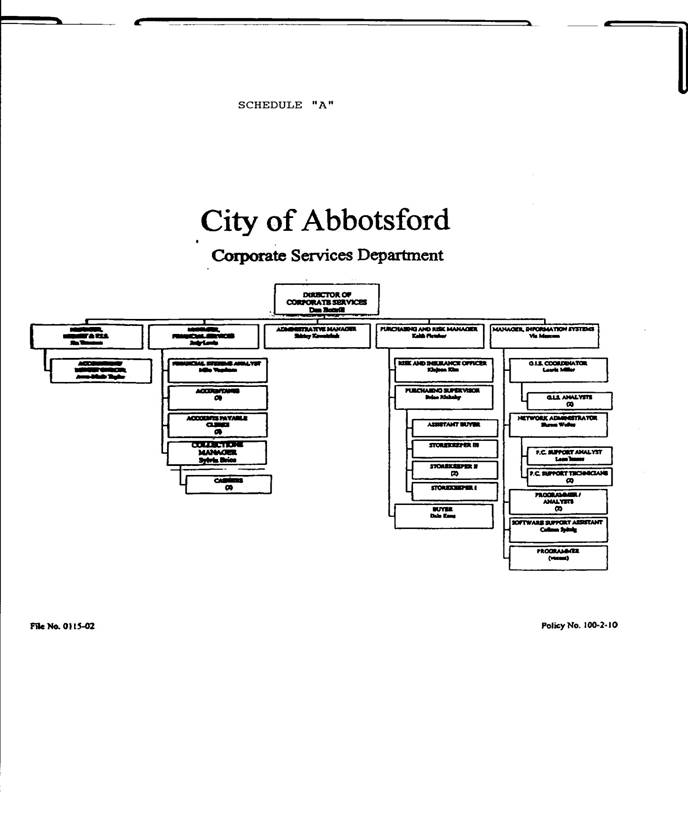

[1] This is an action for damages arising out of a claim of constructive dismissal of Mr. Trueman from his employment with the defendant City of Abbotsford (the “City”).

[2] The City applies under Rule 18A of the Rules of Court to have Mr. Trueman’s claim dismissed. In turn Mr. Trueman applies for judgment on his claim.

[3] The issues to be determined are as follows:

a) Did the City substantially alter Mr. Trueman’s terms of employment so as to result in his constructive dismissal?

b) If so, what was the appropriate notice period that Mr. Trueman was entitled to from the City and what are his damages in lieu of that reasonable notice?

c) If Mr. Trueman has been constructively dismissed, has he mitigated his damages?

The Facts

[4] Mr. Trueman joined the City on January 1, 1995 when the District of Matsqui and the District of Abbotsford amalgamated to form the City of Abbotsford.

[5] Mr. Trueman had formerly been the Deputy Treasurer of the District of Matsqui, a position that he had held since 1980.

[6] When Mr. Trueman joined the City on January 1, 1995 he did so under a written employment agreement with the District of Abbotsford and the District of Matsqui appointing him to the position of Manager, Budget and Financial Systems. The agreement contained a provision stating that:

6.1 The Employee must report to the Director of Finance as designated by Council policy, and will be subject to the instructions and control of the Director of Finance.

[7] Mr. Bottrill had been the Deputy Treasurer with the District of Abbotsford until 1995 and on amalgamation became the Director of Finance for the City. In that position he was responsible for the Finance Department and responsible for the two primary functions of Finance and Purchasing. His responsibilities for Finance included overseeing the City’s budgeting process which Mr. Trueman was to manage.

[8] On January 5, 1996 Mr. Trueman’s responsibilities as Manager, Budget and FIS (Financial Information Systems), were set out in a written job description that directed him to report to the Director of Finance and to supervise a Budget Officer and coordinate with all City departments.

[9] His general accountability was described as follows:

This is a professional accounting position responsible for planning, organizing and coordinating the operation of the Budget Division in accordance with departmental policies and requirements. The Budget & Financial Information Systems Manager is responsible to oversee and coordinate the City budget process and to develop and maintain a financial information’s system that provides accurate, relevant and timely financial data to the various departments in the City. The individual is further responsible for providing internal financial statements and reports in accordance with generally accepted accounting principles which meet the requirements of City Council, Department Directors and Managers.

[10] His key responsibilities were specified as follows:

Manages the operation of the Budget Division.

Responsible for the City budget process including system development, training and review and analysis of departmental submissions.

Monitors variances of expenditures to budget and liaises with departments on a regular basis to deal with current or potential overbudget situations.

Prepares budget documents for Council and public distributions well as news releases.

Responsible for the preparation of the annual operating and the five year capital budget bylaws and subsequent amending bylaws.

Develops and maintains long term financial plans and related comprehensive forecasting models.

Recommends financial policy regarding replacement reserves for physical properties and related rate schedules.

Recommends and implements improved accounting practices and procedures.

Responsible for preparation of interim internal financial statements.

Analyzes financial information and prepares a variety of reports to Council and Director of Finance.

Responsible for preparation of grant applications and claims.

Assists in the preparation of annual financial statements subject to external audit.

Hires, disciplines and terminates employees in the Budget Division as necessary.

[11] In the year 1996 Mr. Bottrill became responsible for the Information Systems Division as well and, in the year 2000 the Human Resources Division was also added to his responsibilities. The name of his department changed from the Finance Department to the Corporate Services Department with Mr. Bottrill changing title to Director of Corporate Services.

[12] The organizational chart at that time appears as Schedule A to these reasons.

[13] When Mr. Bottrill took on the additional responsibilities for the Divisions of Information Systems and Human Resources he says that he had to begin delegating a number of his functions that he had been performing himself and that by early 2002 he had delegated to Judy Lewis, the Manager of the Financial Services Division, many of the financial responsibilities that he had originally handled himself, although he maintained overall supervision and control as the Director of Corporate Services.

[14] When amalgamation occurred in 1995 the City had adopted Matsqui’s Financial Information System (“FIS”) which needed updating. As Mr. Trueman had the responsibility for developing and maintaining the financial system as part of his job requirements, he chaired a committee that evaluated new software and recommended the purchase of a software system called SAP, and he acted as the City’s project manager during implementation of that system and again years later during a major upgrade of that system.

[15] Mr. Trueman’s evidence is that during the final three years of his employment he managed the day to day sustainment of the SAP system. He says in the last three years of his employment 40% of his responsibilities involved managing the FIS system.

[16] While Mr. Bottrill agrees with Mr. Trueman’s role in implementing the SAP system, he disagrees that it is itself a financial information system. He says that SAP is a software package that has hundreds of applications or modules and these modules were installed in many areas of the City for many uses, including for financial information. Accordingly, while FIS was an element of SAP, SAP had a much broader application than just for FIS.

[17] Mr. Bottrill says that after the SAP system was completely implemented by the end of 1999 the amount of time that Mr. Trueman was required to devote to the City’s FIS decreased considerably and his responsibility for sustainment of the SAP system was limited to the coordination of the FIS.

[18] Mr. Bottrill says that technical support for SAP was always the responsibility of the Information Systems Division while development and changes to the capabilities or capacity of any of the modules was the responsibility of each team lead within each division of the City. He says that Mr. Trueman was not responsible for technical support and he was not responsible for development and changes to the modules other than to his own FIS modules. He was responsible, however, for reviewing all decisions by the team leads to add or change the function of their modules, from the budget prospective.

[19] Mr. Bottrill disagrees with Mr. Trueman as to the amount of time that Mr. Trueman was required to spend managing the FIS once the SAP system was in place. He says it was no more than 10% - 20% of Mr. Trueman’s time.

[20] Mr. Trueman’s response is that he was responsible for managing the SAP system overall and not just the FIS component of SAP and the team leads for each module had to report to him. He was managerially responsible for SAP sustainment, although he agrees he did not provide the technical support personally.

[21] Mr. Bottrill says that as Manager of Budget and FIS Mr. Trueman spent the vast majority of his time, particularly in his last three years, on the City’s budget process and related financial projects.

[22] He says from 1995 onward when Mr. Trueman started his employment with the City, the budgeting process required him to do much more than simply add a percentage to each department’s budget each year. As manager of the City’s budget process he was required to work throughout much of the year with the City’s departments to develop their budget requests for the following financial year. In undertaking this role Mr. Trueman needed to understand the roles and functions of each of the City’s departments.

[23] In particular Mr. Bottrill says that Mr. Trueman’s various responsibilities under the budget project included the following elements:

a) learning about the operations of each of the City’s departments;

b) reviewing requests by various departments for increased expenditures, new services or new positions;

c) meeting with the heads of various departments to assess their requests for inflationary increases or increases to fund new positions or new services;

d) working with department heads on a budget timeline;

e) obtaining information from the various departments on a timely basis; and

f) preparation of draft budgets for review by various department heads.

[24] Mr. Trueman says that it was necessary that his position be directly accessible by and to all of the department heads (example: chiefs of police services, fire services, parks and recreation services, etc.) and other stakeholders (example: citizens at public budget meetings, etc.) to adequately gather their input into the overall budget process.

[25] In his view he was at the centre of the City’s budget process “wheel”.

[26] He says that in or about May 2002 he was informed that the City had decided to change direction and implement a much simpler more streamlined budget process which would require no more than a month or two to complete each year.

[27] He describes the changes as basically comprising a rolling over of the previous year’s budget to the current year and making adjustments for known contractual changes and any new initiatives which City council would support, while summarizing this data into a variety of schedules for various purposes and preparing the budget documents.

[28] He viewed the emphasis as clearly changed from activities that encompassed the development, implementation and evaluation of a plan for the provision of services and capital assets to that of producing budget documents (i.e. from financial planning to financial publishing).

[29] In his view the contrast in terms of time and resources that would be required under the new approach and the former approach would be dramatic.

[30] He viewed the adoption of this alternative approach as the City effectively eliminating the need for both his budget division and his own position. He estimated that once implemented the new approach would effectively eliminate approximately 80% of his previous budget responsibilities.

[31] He says that upon questioning someone at the City of how he would fill his days following these changes he was only told that there would be lots for him to do. However his own belief was that the remainder of his public service would have been limited to various accounting or bookkeeping functions and this was not the reason he had chosen to enter public service in the first place many years prior nor the reason that he had accepted the position of Manager of Budget and Financial Information Systems in 1995.

[32] Mr. Bottrill disagrees with Mr. Trueman’s characterization of the proposed changes. He says that the City was actively seeking ways to streamline the financial planning process, to incorporate strategic and departmental master plans and to place a greater emphasis on the preparation of the financial plan by finance staff instead of operational staff from various City departments.

[33] He agrees that the City did decide to make one change to its budgeting process in May 2002 which he communicated to Mr. Trueman. Prior to that point in time an essential element of the City’s budget process required department and division managers to work with Mr. Trueman over the course of a half year to develop their budgets. However after evaluating its budget process the City decided that it could and should compress the amount of time that department and division managers spent working on their budgets in order to free them up to fulfil their other responsibilities.

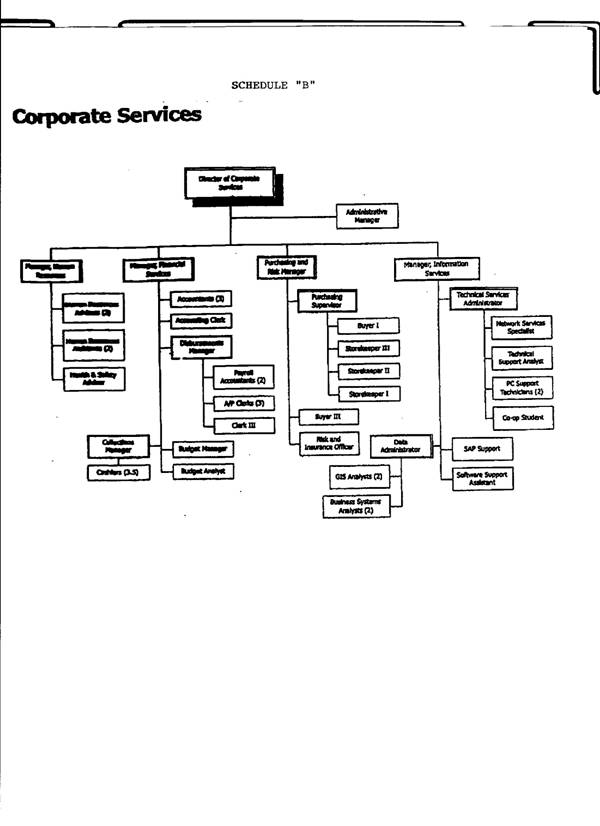

[34] The City therefore decided to place a greater emphasis on preparation of each department or division budget by the City’s financial staff. He says the object was to compress the time that departmental and divisional managers spent preparing their budgets, not to compress the time or effort that Mr. Trueman or his staff would spend. To the contrary, financial staff would prepare the budgets themselves, and then work with department and division heads over a compressed period of time to finalize their budget proposals.

[35] To that end the City decided to merge the Budget Division into the Financial Services Division. Mr. Trueman’s division would be eliminated and Mr. Trueman and his accountant/budget officer would be moved into the Financial Services Division under the direction of Ms Lewis the Manager of Financial Services. Mr. Trueman would maintain his title as Manager of Budget and Financial Information Services.

[36] Mr. Bottrill says that after he had delegated many of his financial functions to Ms Lewis by 2002 in his view her position at that time more closely resembled his original position in 1995 as Director of Finance than did his restructured position as Director of Corporate Services in 2002.

[37] In order to accommodate the new emphasis on the City’s financial staff in the Financial Services Division preparing operating budgets, it was planned to provide additional resources to Mr. Trueman to prepare the budgets within that division. In order to accommodate this, the City had decided that the three accountants already working within the Financial Services Division would work with Mr. Trueman in preparing budgets.

[38] The intention was that the integration of the two divisions would enable the city to ensure its financial planning/budgeting and its financial reporting were consistent.

[39] Mr. Bottrill says that when he met with Mr. Trueman in late May 2002 he reviewed the new emphasis in the budgeting process. He says he told Mr. Trueman that the accountants within the Financial Services Division would be assigned to work with the various departments within the City on their budgets and Mr. Trueman would oversee and supervise their work. He says he told Mr. Trueman at that time that the three accountants in the Financial Services Division would be joined by Mr. Trueman’s assistant from his division, Ms Taylor, his accountant/budget officer.

[40] The three accountants had been reporting to Ms Lewis, the Manager of Financial Services. In addition to their budgeting responsibilities the three individuals would be required to maintain other responsibilities throughout the year and accordingly they would continue to report to Ms Lewis. However Mr. Bottrill says he told Mr. Trueman that he would oversee and supervise their work with respect to the preparation of the budgets.

[41] He told Mr. Trueman that as a result of this integration he would report to Ms Lewis rather than directly to him as Director of Corporate Services but that all other aspects would remain the same in that he would still have the same responsibilities, the same title and the same salary. No other changes would be made.

[42] He says the intention was that Mr. Trueman’s assistant, Ms Taylor, would become one of the accountants in the Financial Services Division and would report to Ms Lewis as well but Mr. Trueman would oversee her work as well as the work of the other accountants with respect to the budgeting process.

[43] Mr. Bottrill acknowledges that Mr. Trueman would lose the ability to “hire and fire” the one staff member who had been in his division, being Ms Taylor, but says in reality he would lose very little since any hiring or firing decisions had to be approved by him and by Human Resources in any event.

[44] Ms Taylor ultimately declined the move into the Financial Services Division and the City paid her a severance package. Mr. Bottrill says that the City believed that this new position for her would constitute a constructive dismissal of her and so a severance amount was paid.

[45] Mr. Bottrill says that Mr. Trueman only raised two objections with him during their meeting. Mr. Trueman was emphatic he did not want to report to Ms Lewis and that he would prefer to report to Mr. Bottrill directly during his remaining time at the City that he expected to be for another two years. Mr. Trueman also expressed a concern that the City Manager would not support the implementation of a process called Recommended Budget Practices.

[46] Mr. Bottrill could see that Mr. Trueman was distressed by the proposed changes and wrote to Mr. Trueman a letter of May 27, 2002 confirming that Mr. Trueman’s responsibilities, title and salary would not change and expectations for him and his position would not change. The only change would be that he would report to Ms Lewis rather than to him and that change in reporting would ensure that the budgeting and financial services would be fully integrated.

[47] He also let Mr. Trueman know that he was a valued employee of the City and the restructuring was not any reflection upon his performance.

[48] Mr. Trueman says he viewed the proposed changes in a different light. As far as he was concerned his days would be mostly restricted to interacting with finance department accounting staff who had no expertise in budget matters, and assisting them with the preparation of the budgets and his days of being able to spend the majority of his time interacting with departmental brass was clearly over. He considered this to be a very dramatic and totally unsatisfactory change to the responsibility or character of his employment function and he was terribly disappointed that his purpose with the City would be reduced so low.

[49] In answer to Mr. Bottrill’s statement that departmental and division managers had been spending time working on budgets instead of fulfilling their responsibilities, Mr. Trueman responds that the budget process was the planning process and the planning process was their responsibility.

[50] He viewed the changes as removing participation in and responsibility for the budget process from the departmental and division managers and turning that responsibility over to the Finance Division staff, while at the same time wiping out his Budget Division and his staff and transferring him to a non-managerial staff role in the Financial Services Division. In his view his year long budget responsibilities were most certainly diminished by a serious and substantial amount.

[51] He also disagrees with Mr. Bottrill’s statement that he had transferred most of his financial responsibilities to Ms Lewis as in his opinion Ms Lewis’ position of Manager of Financial Services was not even remotely comparable to Mr. Bottrill’s position as Director of Finance in 1995. Mr. Bottrill never transferred his management responsibilities and Ms Lewis was never given his executive responsibilities.

[52] Mr. Trueman viewed the budget process as having been reduced to a part-time accounting/clerical exercise. He did not consider that this was contemplated by the terms of his employment. In his view he had lost “ownership” of the Budget Division, the Budget Division staff, the budget process, the SAP system, and any semblance of any real managerial responsibility.

[53] He disputes Mr. Bottrill’s statement that the City intended to move his assistant, Ms Taylor, over to the Financial Services Division as well as he says he was informed that Ms Taylor had been bought out and was not going to continue her employment with the City. Accordingly Mr. Bottrill never discussed with him the idea that Ms Taylor would continue with him in the Financial Services Division.

[54] Mr. Trueman seriously disputes Mr. Bottrill’s view that other than the change of reporting level all other aspects of his job in terms of responsibilities, title and salary, would remain the same.

[55] He points out that following the termination of his employment the organizational chart for the Corporate Services Division indicated that his title was changed to only Budget Manager and the SAP/FIS responsibilities were transferred to the Information Services Division.

[56] Mr. Trueman says that in the final two years or so of his employment he had been recommending that the City establish an in-house sustainment team for the SAP system utilizing the considerable talents of two of the members of the SAP implementation and upgrade teams but the recommendation was met with considerable resistance within the City.

[57] However, he says in May 2002 Mr. Bottrill instructed the Manager of the Information Services Division to invite an outside consultant, Telus, to propose a contractual arrangement for the provision of sustainment services.

[58] In his affidavit of November 9, 2005 Mr. Trueman says this decision was made without his knowledge or participation. He does acknowledge that during the week of May 18, 2002 he was invited to sit in on a presentation by the consultant but he says he was extremely surprised that he was left out of the decision making process in regard to this matter that he considered to be one of his key responsibilities.

[59] However a week later when his division was dissolved and he was to be transferred to the Financial Services Division he says it became clear to him that this activity was part of a plan to migrate or transfer management of the Financial Information Systems (i.e. SAP) to the Manager of Information Services and reduce his responsibilities accordingly.

[60] In his affidavit Mr. Bottrill denies that there was any plan at that time to transfer management of the Financial Information Systems from Mr. Trueman to the Information Systems Division or anywhere else within the City or to a consultant.

[61] He also denies that Mr. Trueman was left out of the discussions with Telus as the outside consultant. He says that Telus had approached the Manager of the Information Systems Division, Mr. Morcom, with a proposal to provide an assessment of the SAP system free of charge and the City agreed to accept that proposal. Telus was to perform the assessment with the objective of then making a proposal to the City to provide services to support and maintain the City’s SAP system for a five year period but the engagement letter with Telus put no requirement on the City to enter into any services agreement after Telus delivered its assessment.

[62] Mr. Bottrill says that after Telus delivered its assessment and after the City had reviewed Telus’s proposal to provide SAP support services over a five year period, the City decided not to accept Telus’s proposal.

[63] Mr. Bottrill also says that Mr. Trueman was quite aware that Telus was assessing the City’s SAP system and was a direct party to those discussions.

[64] In his subsequent affidavit of October 8, 2006 Mr. Trueman reiterates that Mr. Morcom never came to him to inform him of these discussions with Telus for which he had managerial responsibility at the time and the first time that he became aware of the events was through Mr. Bottrill’s affidavit.

[65] This repeated denial by Mr. Trueman prompted Mr. Morcom to depose an affidavit of October 20, 2006 attaching a number of internal emails that clearly indicates that Mr. Trueman was involved in the Telus proposal before he left the City and was not objecting to it.

[66] This led to a concession at the hearing by counsel for Mr. Trueman that in fact Mr. Trueman was directly involved at that time.

[67] However Mr. Trueman says that contrary to Mr. Bottrill’s statement that there was no intention of moving the SAP/FIS responsibilities from him, subsequent to his termination the manager of the Information Services Division did in fact assume managerial responsibility for the SAP system.

[68] Mr. Bottrill’s answer to this is that sometime after Mr. Trueman had left the City Mr. Morcom suggested that the City should add capacity in house for SAP sustainment and Mr. Bottrill agreed and therefore in mid-2003 the City hired an SAP business analyst as a full-time consultant. One year later when this individual came on staff, the reporting was to Mr. Morcom in the Information Services Division.

[69] Mr. Bottrill says that the SAP support person does not perform the duties that Mr. Trueman had performed as Mr. Trueman never had the same type of responsibilities.

[70] The organizational chart for the Corporate Services Division as of 2004 appears as Schedule B to these reasons.

[71] Mr. Trueman took a leave of absence commencing May 29, 2002 to consider the changes and his position. Mr. Bottrill says that during subsequent meetings through June 2002 with Mr. Trueman he never complained about any loss of responsibilities or about not being able to attend regular management meetings in the future. He only complained about having to report to Ms Lewis and his concern that the City would not adopt the Recommended Budget Practices.

[72] Mr. Bottrill says that Mr. Trueman was well regarded within the City and he tried to persuade Mr. Trueman to stay. He says Mr. Trueman enjoyed the respect of his colleagues for his skill in budgeting. Mr. Bottrill was satisfied that Mr. Trueman’s working conditions would not have been substantially different or demeaning and his relationships with his colleagues in Corporate Services would have remained professional and cordial.

[73] Mr. Trueman considered his position through the month of June 2002 and on July 2, 2002 Mr. Lundquist, the Human Resources Manager, wrote Mr. Trueman on behalf of the City indicating that the City had to bring the issue to a conclusion. He asked Mr. Trueman to contact him if Mr. Trueman intended to retire but if the City did not hear from Mr. Trueman by the following day, July 3, 2002, the City would consider that Mr. Trueman was claiming constructive dismissal and his employment would be terminated as of that day.

[74] When Mr. Trueman did not reply by July 3rd, on July 8, 2002 Mr. Lundquist confirmed by subsequent letter to Mr. Trueman that he had elected to claim constructive dismissal and had terminated his employment effective July 3, 2002.

[75] Following Mr. Trueman’s termination of employment Mr. Bottrill says that in February 2003 the City hired Ms Sinclair as its Manager, Budget and FIS and she had the same title as Mr. Trueman held and the same responsibilities for budgeting and financial information systems until she moved to a different position in the City.

[76] He says that she worked with the accountants in the Financial Services Division in preparing the budgets for each of the City’s departments and she met with those accountants on a regular basis to discuss upcoming issues and supervise their work.

[77] While she had a direct reporting relationship with the Manager of Financial Services she also attended meetings with him as the Director of Corporate Services and with other departmental managers when they met to discuss financial planning. She was always in attendance at the City manager and directors meetings when financial planning matters were discussed. Her successor has the same rights and Mr. Trueman would have had these same rights as well.

[78] In his view when Mr. Trueman describes himself as having been at the centre of the City’s budget process wheel in that it was necessary that he be directly accessible by and to all of the City’s department heads and that he report directly to senior management, this is an accurate description of the role of Ms Sinclair and her successor as Budget Manager. She continues to deal directly with department heads on a regular basis with or without the accountants in Financial Services Division. She consolidates and coordinates all the elements of the budget process and in that sense is very much still at the centre of the wheel of the City’s budgeting process.

[79] Mr. Trueman says that while the present Budget Manager may be allowed to attend the Corporate Services Department Managers Meeting when financial planning is to be discussed, in his former position as a division manager he was entitled to attend all meetings by right. He views the current Budget Manager as only a “false manager” in that she has no true managerial responsibility and has no staff directly reporting to her.

Analysis - a) was Mr. Trueman constructively dismissed?

[80] Mr. Trueman joined the City in 1995 under an employment agreement that appointed him to the position of Manager, Budget and Financial systems. He was required to report to the Director of Finance and subject to the instructions and control of that Director, who was Mr. Bottrill. His job description required him, inter alia, to manage the operation of the Budget Division.

[81] In May 2002 the City proposed to eliminate the Budget Division and fold the Division, Mr. Trueman and his assistant into the Financial Services Division. Mr. Trueman was to retain the same title of Manager, Budget and FIS as well as the same salary and benefits, but he was to be required to report to the Manager of Financial Services, Ms Lewis, rather than to Mr. Bottrill as the Director.

[82] In addition, Mr. Trueman’s assistant was to become another accountant in the Financial Services Division who would report to Ms Lewis rather than to Mr. Trueman, although Mr. Trueman would supervise her work. The other accountants in the Financial Services Division would also work under the supervision of Mr. Trueman on budget matters but otherwise would attend to other duties in the Division and would also report to Ms Lewis as the Division Manager.

[83] The issue for determination is whether these changes were substantial changes to essential terms of Mr. Trueman’s employment such that they amounted to a fundamental or substantial change to his contract – changes that violated the terms of his contract going to the root of the contract so as to render future performance of the contract a thing different in substance.

[84] If the City committed a fundamental breach of the contract, then the contract was at an end and Mr. Trueman was entitled to consider himself constructively dismissed (Farber v. Royal Trust Co., [1997] 1 S.C.R. 840; Poole v. Tomenson Saunders Whitehead Ltd., [1987] B.C.J. 1664 (B.C.C.A.)).

[85] If Mr. Trueman cannot satisfy his onus to prove that there was a fundamental breach of his contract, then he has not been constructively dismissed, and by refusing to return to work under the changes he has effectively resigned from his employment and is not entitled to any future employment benefits or any damages in lieu of reasonable notice.

[86] Many of the cases cited to me involve circumstances where the employee began the employment in one position and moved into other positions before the issue of constructive dismissal arose when he/she refused to move to yet another position.

[87] In those cases the terms of the contract may not have entitled the employee to remain in any particular position so that he/she could be transferred to other positions without there being any breach of the employment contract in that regard, even if the new position was one of less prestige.

[88] In those cases it was a question of whether a change of duties upon transfer constituted a fundamental breach of the employment contract, regardless of the loss of prestige.

[89] Those cases are to be compared to other cases where the employee has contracted with the employer to perform the duties of a specific position with a certain level of prestige. One such case was O’Grady v. ICBC, [1975] 63 D.L.R. (3d) 370 (B.C.S.C.) where Mr. O’Grady had contracted for a specific position and was constructively dismissed when it was proposed he move to another position that was clearly subordinate with quite different duties from those he had contracted to perform and with less prestige.

[90] This case is more like Mr. O’Grady’s case in that Mr. Trueman contracted initially for the specific position of Manager, Budget and FIS with certain specified and documented responsibilities and a certain level of prestige, and the question is whether the proposed changes amounted to a breach of the terms of his contract going to the root of the contract.

[91] In my view there must be less discretion for the City in this case where the term of the contract at all times was to employ Mr. Trueman in a specific position as Manager of Budget and FIS with specific job responsibilities. However the question still remains whether the changes constituted a fundamental breach of his contract.

[92] With respect to the key responsibilities set out for Mr. Trueman in his written job description, Mr. Trueman says that his responsibility and authority to “manage the operation of the Budget Division” and to “hire, discipline and terminate employees in the Budget Division as necessary” have been lost to him when the entire Budget Division was eliminated and he was made just another employee of the Financial Services Division, without any authority to hire, discipline and terminate any other employee.

[93] In his examination for discovery Mr. Trueman agreed that his other responsibilities set out in the job description would have remained with him.

[94] I understand Mr. Trueman’s central complaint to be that he would no longer manage a division and be equal to all other division managers in the Department of Corporate Services, with the right to report directly to Mr. Bottrill as the Director and the right to attend meetings of division managers and deal with those division managers directly on budgeting issues. What he envisioned with the change was a loss of his division, a loss of contact directly with Mr. Bottrill because he was required to report to Ms Lewis in the Financial Services Division, and a loss of direct contact with other division managers on budget planning issues, because they were to become less directly involved personally as they and their staff would be meeting with Financial Services staff who would in turn report back to Mr. Trueman on budget matters. He did not see his involvement personally as involving more than two months of his time in any year.

[95] I do not see Mr. Trueman’s loss of authority to hire and fire as being any fundamental breach of his contract as he only ever had the right on paper to hire, discipline or fire one employee in his division, Ms Taylor, and his right to hire and fire was only ever a theoretical right because in reality the right to hire and fire remained ultimately with Mr. Bottrill as the Director and with the Human Resources Manager.

[96] Mr. Trueman would have remained in charge of preparing the budget. He would also have retained his title as Budget Manager. More than the title he would have truly remained the budget manager in the sense of being primarily responsible for budget preparation and planning. He would have continued to manage in fact the accountants in the Financial Services Division on the budget who were obtaining information from other departments for the budget. He would have lost his own division however and the prestige of reporting to the Director rather than to the Financial Services Division Manager.

[97] I accept as well that Mr. Trueman would not have had the same degree of contact on budget matters with other division managers because the City had directed that they no longer be as involved as before. However, it was never part of Mr. Trueman’s stated job description responsibilities to necessarily be entitled to interact directly with other division managers.

[98] It is true that prior to the change Mr. Trueman’s responsibilities under the budget process included meeting with department heads to assess their requests for increases to fund new positions or new services, working with department heads on a budget timeline and preparation of draft budgets for review by various department heads. Mr. Bottrill has confirmed that in his affidavit evidence.

[99] However a change in the manner in which Mr. Trueman is to carry out his employment responsibilities, as opposed to a change in those employment responsibilities themselves, cannot constitute a fundamental change to his contract of employment.

[100] Mr. Bottrill says that Mr. Trueman’s successor is still involved in meetings with him and other division managers and at the directors’ meetings where financial planning is discussed, and the successor also deals directly with division heads on a regular basis as she consolidates and coordinates all the elements of the budget process.

[101] Mr. Trueman says he had all of these avenues open to him as of right when he was a division head and not as a matter of permission only, with the budget manager needing to be involved in planning the budget in addition to preparing the budget.

[102] However, I conclude that Mr. Trueman would have had the same opportunities and responsibilities as his successor presently has, if he had stayed on in that position and I accept that the City had the right to decide the degree of participation of its managers in the budget without there being any breach of Mr. Trueman’s contract.

[103] So what is left for consideration is the loss of Mr. Trueman’s Division and the loss of his right to report directly to Mr. Bottrill.

[104] I do not know if Ms Lewis had the same stature in financial matters in 2002 as Mr. Bottrill had in 1995, but she definitely was not at the top of the pyramid in the Corporate Services Department, as Mr. Bottrill was. Mr. Trueman would have been required to report to a lower level.

[105] In Moore v. University of Western Ontario (1985), 8 C.C.E.L. 157 (Ont. Sup. Ct.) the plaintiff had a contract to be the Director of the Department of University Relations and Information and a requirement to report to the President. Under a major reorganization he was required to report to an Assistant Vice-President who in turn would report to a Vice-President who would report to the President. The court said that reporting status by itself is not the sole criteria to determine the stature of a job or position. There was still access to the President allowed and it was determined that there was no fundamental breach to the plaintiff’s contract.

[106] In Poulos V. Murphy Oil Co. Ltd., [1990] 5 W.W.R. 696 (Alta. Q.B.), the plaintiff was a manager of a department in an oil company who, along with a number of other managers of departments, some of them being vice-presidents, reported directly to the President. After reorganization the plaintiff’s department was folded into another department headed by a vice-president and she was required to report to him. However her title and responsibilities did not change.

[107] The plaintiff had had the authority to write her own job description before the reorganization and it called for her to report to the President. She regarded this direct access to the President as being of importance to her.

[108] The court concluded that there was some loss of stature for her, as a division head reporting to a vice-president does not enjoy the same hierarchal status as a department head reporting directly to the president. The court considered this to be a unilateral change imposed on the employee when her department became a division of a vice-president’s department and when she reported to him rather than the president, but otherwise substantially retained all other rights and responsibilities with respect to her employment.

[109] The court concluded that there was no doubt the change in reporting was of significance, but it did not go to the root of her contract when everything else remained substantially the same. Accordingly she was not constructively dismissed.

[110] Similarly here, I conclude that the unilateral change in Mr. Trueman’s reporting requirements together with the loss of his division do not constitute a fundamental breach of his employment contract, when everything else remained substantially the same. He was still the Budget Manager, he was managing the employees in the Financial Services Division who were reporting to him on budget matters and he still had the opportunity to meet with other managers and with the director on budget planning issues as his successor has enjoyed.

[111] I do conclude that Mr. Trueman would have lost some stature as he would no longer have been a division manager but on the evidence I conclude that this would have been mostly in his mind and would not have occurred in fact when he continued to assume the same responsibilities.

[112] I conclude that Mr. Trueman was precipitous in resigning without determining how the changes would in fact affect his responsibilities as it appears from the evidence that they would not have been substantially affected.

[113] I do not accept that the City planned to transfer Mr. Trueman’s SAP responsibilities away from him, to Mr. Morcom, before Mr. Trueman’s employment terminated. Mr. Trueman put his belief in the fact that Mr. Morcom was dealing with Telus on SAP sustainment and not involving him. However, it turns out that Mr. Trueman was intimately involved at that stage and so the basis for his stated belief about a transfer proposed, has disappeared.

[114] It may be that the SAP system was subsequently transferred to Mr. Morcom’s division in 2003 but I accept Mr. Bottrill’s evidence that the idea only came up after Mr. Trueman had left the City and I do not consider that event to be relevant to the circumstances of Mr. Trueman’s termination.

[115] I conclude that Mr. Trueman was not constructively dismissed.

[116] I conclude that Mr. Trueman effectively resigned by not returning to work to perform his responsibilities. As he has resigned and not returned he is not entitled to any continuing employment benefits or to damages in lieu of notice of termination.

[117] In view of my conclusion that Mr. Trueman was not constructively dismissed there is no need for me to consider the two remaining issues.

[118] The claim is dismissed. The City will have its costs at Scale 3.

“J. Truscott, J.”

The Honourable Mr. Justice J. Truscott